Gold will navigate near-term headwinds to reach $5,000oz by year-end – ING’s Manthey

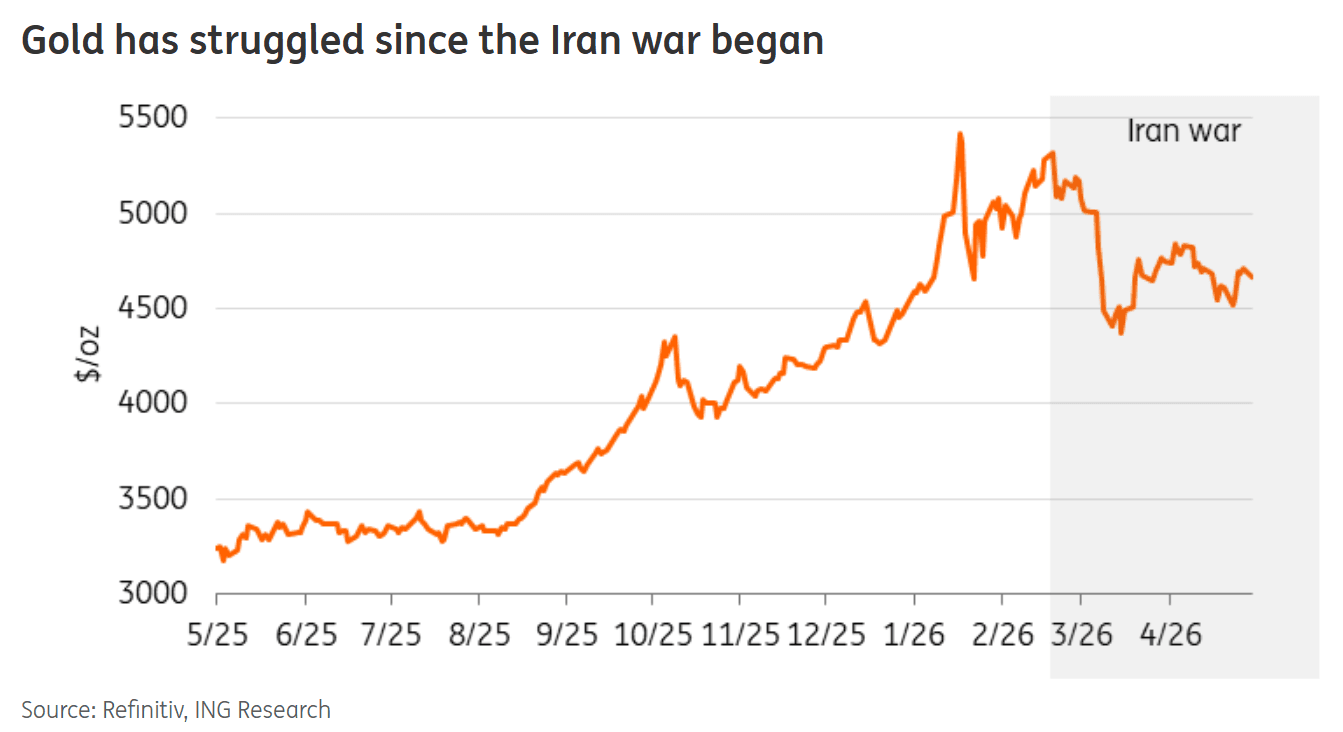

Even though gold has lost around 12% of its value since the Iran conflict began, the sell-off only reflects the macroeconomic impacts of the oil price shock rather than a breakdown in gold’s safe-haven role, according to Ewa Manthey, commodities strategist at ING.

“Gold’s safe-haven appeal tends to perform best in a financial crisis or growth shock – when real yields fall and the dollar weakens,” she wrote. “A supply-driven energy shock does the opposite. Higher oil prices push inflation up, keep central banks on hold and strengthen the dollar, all of which weigh on gold. High liquidity also makes it a source of funds when investors need to cover losses elsewhere.”

Manthey said markets saw the same dynamic in 2022 after Russia invaded Ukraine. “After an initial rally, gold came under pressure as the inflationary impact of higher energy prices pushed yields and the dollar higher,” she said. “The same dynamic has played out here, only faster.”

Manthey said the yellow metal is facing a number of headwinds at the moment.

“The Federal Reserve left rates unchanged in April and the tone from Chair Jerome Powell was cautious,” she noted. “Inflation has re-accelerated since the war began and the case for near-term easing has weakened. Our US economist still expects easing in the second half of the year, but a prolonged energy shock could push that back. Real yields and the dollar remain the key constraints on gold.”

Gold has also given back some of last week’s gains following President Trump’s rejection of Iran’s latest proposal. “The setback keeps the ceasefire timeline uncertain and inflation risks elevated – reinforcing the higher-for-longer rate narrative that has weighed on gold throughout the conflict,” she wrote. “A durable resolution remains the key catalyst for a sustained gold recovery. On the macro side, Friday’s payrolls data showed employers added jobs for a second consecutive month in April and unemployment held steady at 4.3%. That gives the Fed little reason to rush on cuts, keeping yields and the dollar as near-term headwinds for gold.”

Manthey noted that this week’s inflation data could serve to reinforce this stance on the part of the central bank. “Powell’s tenure ends this week, adding another layer of uncertainty around the Fed’s independence.”

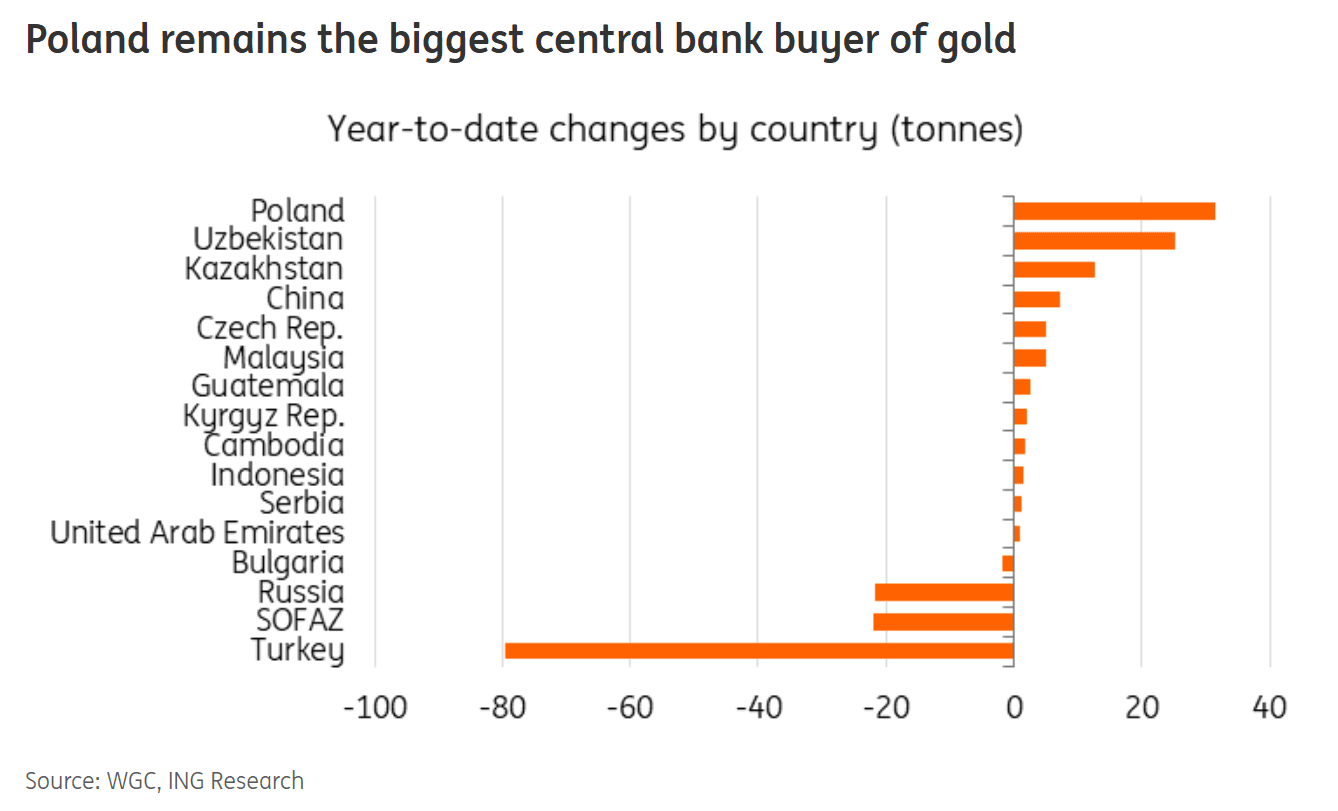

Central bank demand, however, continues to underpin the gold market. “China’s central bank returned to buying in April, adding 8.1 tonnes – the most since December 2024 – extending its buying streak to 15 consecutive months and lifting total holdings to around 2,305 tonnes,” she noted. “Overall, although central banks turned net sellers of gold in March, with net sales of around 30 tonnes, purchases in the first quarter still totalled 27 tonnes, according to data from the World Gold Council. Turkey led the selling, cutting holdings by 60 tonnes as part of efforts to support FX liquidity, taking its first quarter net sales to 79 tonnes. Buying remained concentrated, with Poland adding 11 tonnes in March and 31 tonnes year-to-date.”

Manthey pointed out that central bank demand was up 17% quarter-on-quarter in Q1 despite the uptick in sales, with Poland and Uzbekistan leading the purchases. “The National Bank of Poland was once again the largest purchaser, increasing its gold reserves by 31 tonnes over the quarter to 582 tonnes,” she said. “Despite recent statements by Governor Adam Glapiński about the possibility of selling some of its gold, the central bank appears to remain focused on reaching its 700 tonne target.”

Despite the large gold sales by Turkey and Russia, the data still support “a slower but still positive trend in official sector demand, with reserve diversification remaining supportive for gold over the medium term.”

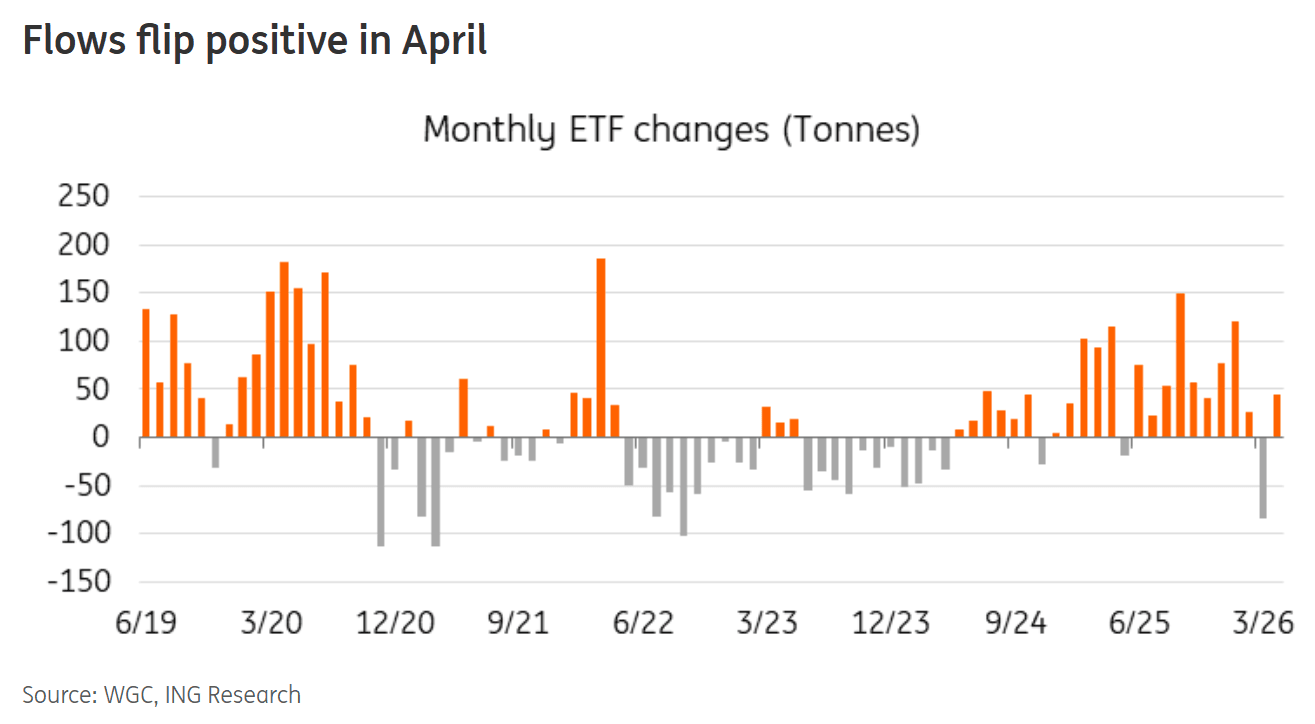

Fund flows, which have not been price-supportive since the outbreak of the Iran conflict, have also started to turn.

“ETF outflows have weighed on prices since the conflict began, unwinding much of this year’s previous inflows,” Manthey said. “Early signs suggest positioning is beginning to shift. Global gold ETFs recorded roughly $6.6bn of inflows in April, flipping from March outflows, according to World Gold Council data, with Europe leading the move, reflecting concerns that the region would be more exposed to a Strait of Hormuz closure. Contributions from Asia and the US were around a third of Europe’s over the month.”

Manthey noted that ETF holdings remain well below the November 2020 peak, suggesting there’s room for a significant rebuild. “ETF flows track Fed expectations closely – Fed easing should be a catalyst for renewed inflows in the second half,” she said.

“Meanwhile, COMEX managed money net longs continue to point to a constructive investor backdrop, though positioning has yet to reach crowded territory.”

Manthey said ING remains constructive on gold, but the bank acknowledges that the stalled peace talks add near-term uncertainty. “Trump’s rejection of Iran’s latest proposal keeps the ceasefire timeline unclear and inflation risks elevated, which limits the Fed’s room to cut,” she said. “The path higher depends on energy prices easing, inflation cooling and the Fed cutting in the second half of the year. Central bank buying and recovering ETF flows provide additional support.”

ING now projects the gold price to reach $5,000 per ounce by the end of the year. “The main downside risk is a breakdown in peace talks that keeps energy prices elevated and the Fed on hold into year-end,” she said.

Manthey reiterated that despite the near-term headwinds, gold’s safe-haven role is not in question. “However, recent months have shown that short-term price action can still be dominated by macro forces – particularly real yields, the dollar and expectations for Fed policy,” she said. “Once those headwinds begin to ease, gold's underlying support should reassert itself.”